The Property I Filmed Two And A Half Years Ago

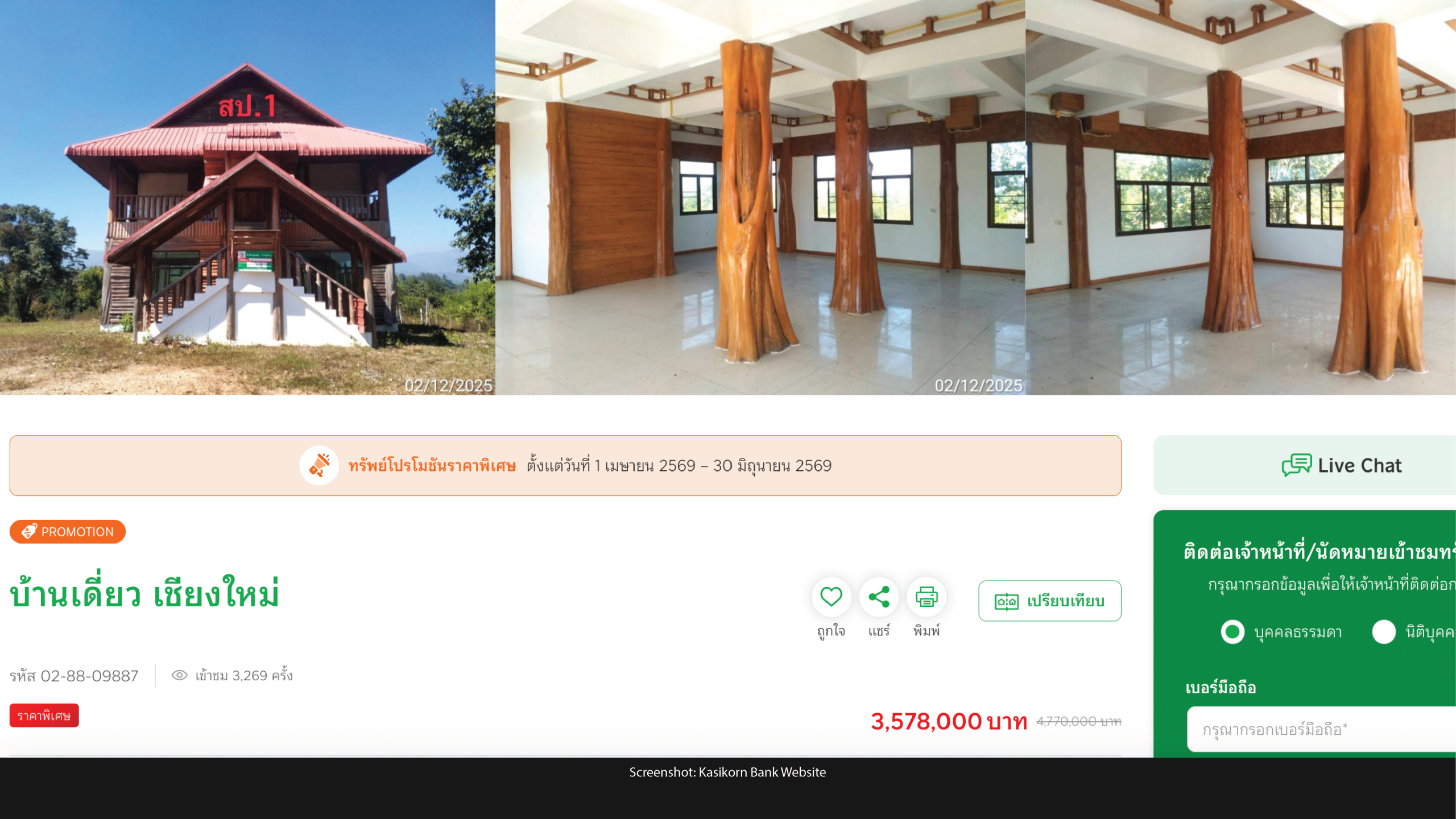

Two and a half years ago, I filmed a video about foreclosed properties in rural Thailand. It was about a property listed on the Kasikorn Bank website. A foreclosed house, for the “Special promotional price” of 3.5 million baht.

That same property is still listed today. Same listing. Same bank. Same house. Same “special promotional price.” Two and a half years later. The price has dropped by 40,000 baht. Forty thousand. On a 3.5 million baht asset. Barely one percent. A “special promotion” that has been running longer than most tenancy agreements. That house has been sitting empty for at least two and a half years. The roof leaking. The garden growing over. The market around it getting worse, not better. And the bank’s response to all of that is to knock off an amount that would not cover a month’s rent and keep calling it a special offer.

Before The Thailand Apologist Tells Me This Is One Unlucky House

And before Mr Thailand Apologist tells me that is just one unlucky house in a bad location, I lived twenty kilometres from this property. I drove past it. There is nothing wrong with it. It is a normal house in a normal part of rural Chiang Mai. Nobody is buying it because the price has nothing to do with what the house is worth and everything to do with what the bank needs it to be worth to stop the whole thing from collapsing. And I know that because of the second property. Also documented at the time on the old channel, the recording is public again too with the link in the description. This one is my favourite. Because someone at the bank looked at a foreclosed house that had been sitting unsold and arrived at a conclusion that could only make sense inside a Thai bank. The problem is the price is too low. So they raised it. They took a repossessed property that nobody wanted and made it more expensive. And it will not surprise you to learn that the house is still there. Still unsold. Still empty. Still deteriorating. Just costs more now than when nobody was buying it the first time.

Seven Out Of Eleven Properties Still Sitting On The Same Bank Website

But it is not just two. I documented eleven foreclosed properties on the old channel. I have made every single one of those recordings public again. The links to the original bank listings still work, you can check them yourself, right now, today. Of those eleven properties, seven are still listed for sale. Same prices. No meaningful change. Two and a half years later. Seven out of eleven still sitting there, unsold, at prices the market has walked away from.

The other four are gone from the listings. Maybe they sold. Maybe the original owner clawed them back. Maybe the bank quietly removed them because they had been sitting there so long they were becoming embarrassing. I do not know. But I know that seven out of eleven is not a coincidence. It is not a bad location. It is not a pricing error. It is a pattern. And it is a pattern that exists because the banks cannot afford to drop the prices to where someone might actually buy, because doing so would mean booking losses they are not prepared to admit.

Same bank. Same website. Seven properties frozen in time. The market is not being allowed to correct. The prices stay where the bank needs them, not where the market wants them. And the crisis stays hidden, not because it is not happening, but because the numbers on the website are a fiction designed to disguise how bad things actually are.

How Bad Things Actually Are In Thai Property

So let me show you how bad things actually are.

I have been watching this for three or four years. The eleven I documented are from Kasikorn Bank alone, one bank. But there are dozens of other banks doing exactly the same thing. Bangkok Bank. Krungsri. SCB. Krungthai. Government Savings Bank. Every single one of them has a property division selling homes that used to belong to Thai families who could not keep up with the payments. And when you start looking, really looking, at the volume of what is out there, something becomes very clear. This is not a healthy property market offering good deals. This is the wreckage of a debt crisis that has been quietly destroying rural Thailand for years. And the “cheap property” that every expat writer tells you about is not cheap because Thailand is a bargain. It is cheap because Thai people are losing their homes. And even then, it is not cheap enough, because the banks will not let the prices fall to where they should be.

The Real Number On Thai Household Debt

Thailand’s household debt stands at 16.3 trillion baht. That is roughly 470 billion dollars. As a percentage of GDP, the official figure sits at around 87 percent. That is already one of the highest ratios in the world, seventh globally. Higher than Malaysia. Higher than Hong Kong. Higher than most countries with far more developed economies.

But that is the official number. The real number is worse.

A study by Chulalongkorn University, commissioned by the Joint Standing Committee for Commerce, Industry and Banking, found that when you include informal loans, the borrowing that never appears in any bank’s records, Thailand’s household debt reaches 104 percent of GDP. Forty percent of Thai households have informal debt. The average informal debt per household is nearly 100,000 baht. And the interest rates on that informal debt are not 5 percent, not 10 percent, not even 20 percent. Loan sharks in rural Thailand charge up to 240 percent per year. Some charge 20 percent per month.

That is not a debt problem. That is a debt emergency. And it is concentrated exactly where you would expect, in the countryside, among the people with the least protection, the least formal employment, and the least access to the banking system that is supposed to serve them.

How The Thai Foreclosure Trap Actually Works

Here is how it works. And once you understand this, you will never look at a cheap Thai property listing the same way again.

A rural Thai family earns a modest income. Farming, day labour, seasonal work. Their income is irregular. The formal banking system does not want them. Commercial banks have been tightening lending criteria for years, in fact, for the first time in recent history, household lending by commercial banks actually contracted, shrinking by 1.2 percent. Banks are not lending to the people who need it. They are pulling away.

So when something goes wrong, a medical bill, a failed harvest, a motorbike that breaks down and cannot be repaired, a child’s school fees, the family has nowhere to turn except informal lenders. Loan sharks. Pico finance. Neighbours with cash. People who will lend you money at rates that would be criminal in any developed country.

The family borrows. The interest compounds. They borrow more to service the first loan. They fall behind. They cannot catch up because their income has not grown, in fact, for the poorest workers, those earning under 7,800 baht a month, real income has fallen by 18.5 percent since before the pandemic. They are earning less than they were five years ago, in real terms, while their debt stays the same or grows.

Eventually, something has to give. If they were lucky enough to own property with proper title, a house on Chanote land, a plot they could mortgage, the bank takes it. If they borrowed against it, the bank forecloses. The house becomes an NPA, a non-performing asset, and it goes on a website. You have already seen what happens next. The bank overvalues it. The listing sits there for years. The house rots. And the market is not allowed to correct.

The Scale Of Thai Non-Performing Debt

More than 1.2 trillion baht in loans are currently classified as non-performing in the Thai credit bureau system. That is debts more than 90 days overdue. One point two trillion. The government launched a debt-relief programme targeting 3.4 million people with small NPLs, debts under 100,000 baht. Three point four million people. The combined debt value of just that group is 120 billion baht.

And the government’s flagship debt clinic, SAM, Sukhumvit Asset Management, has managed to restructure somewhere between 55,000 and 60,000 cases. Out of millions. The programme barely scratches the surface.

Personal loans have a non-performing rate of 10.77 percent. More than one in ten personal loans in the country is bad. And when people cannot get formal credit because the banks have tightened the taps, they go to the informal market. Shark loans totalled 67 billion baht in the last survey. Nearly half of all informal borrowing, 47.5 percent, was for daily consumption. Not investment. Not a business. Not an asset. Just food. Just getting through the week.

Thai Debt As Cancer, Not As Bomb

Economists in 2026 describe Thailand’s debt not as a bomb that will explode. They describe it as a cancer. Slowly eating away at growth. Slowly eating away at consumption. Slowly eating away at the ability of ordinary people to participate in their own economy. The average Thai office worker now spends 40 to 50 percent of their income on debt interest alone. When half your wage goes to servicing debt, you stop buying clothes. You stop eating out. You stop spending money in the small businesses around you. Those businesses fail. Their owners go into debt. And the cycle continues.

The IMF projects Thailand’s GDP will grow by just 2 percent in 2025 and 1.6 percent in 2026. Near the bottom of ASEAN. The property market is in its coldest period in two decades. Car sales dropped 26 percent in 2024. Tourism, the thing that was supposed to save everything, declined 7.5 percent year-on-year in the first nine months of 2025.

This is not a country in recovery. This is a country where the majority of people are getting poorer while the headline numbers pretend everything is fine.

Why Rural Thailand Is The Worst-Hit

And in the countryside, where the debt is deepest and the protections are weakest, the damage is worst.

Rural Thailand runs on informal employment. More than half of all Thai workers are not formally employed. No contract. No social security. No unemployment insurance. No sick pay. When the harvest fails, and severe drought has been hammering farm incomes, there is no safety net. There is only debt. And the debt, for people in the informal economy, almost never goes through a bank. It goes through someone who charges 20 percent a month and does not accept excuses.

Government debt-relief measures focus mainly on formal-sector borrowers. If your debt is with a bank, there are programmes. If your debt is with a loan shark in your village, you are on your own. The system that is supposed to help does not reach the people who need it most. And the system that does reach them, the informal lending market, is designed to extract, not to support.

When these families finally lose their property, it becomes one of the eleven listings I showed you at the start. Or one of the thousands like them across the country. The family is gone. The debt remains. The house sits empty. And eventually the listing gets shared on an expat Facebook group with a caption that says something like, “Amazing deal, rural Thailand, only 800,000 baht.”

That is not an amazing deal. That is the end of someone’s life as they knew it. And the system that broke them is the same system that will not give rural Thais proper title to the land they have farmed for a century, that charges them interest rates that belong in a loan-sharking prosecution, and that excludes them from formal finance the moment they fall behind, then repossesses their home, overvalues it on a website, and calls it a performing asset until the auditors stop asking questions.

The Question Foreigners Posting About Cheap Thai Property Cannot Answer

I have been watching this for years. Scrolling through the listings. Driving past the properties. Watching the numbers grow. Every major bank in Thailand has a foreclosure division. Every one of them is selling homes, land, and commercial buildings that belonged to people who could not keep up. And every time I see a foreigner post about how cheap property is in Thailand, I think about the family that used to live there.

Because the thing about cheap property is that someone always paid for it. And in Thailand, the people who paid are not the people buying. They are the people who borrowed at 240 percent interest to get through a bad harvest. The people whose real wages have fallen 18 percent in five years. The people who spent half their income servicing debt they took on to feed their children. The people the banking system abandoned and the informal market consumed.

Thailand’s household debt is at 104 percent of GDP. Forty percent of households carry informal loans. More than one in ten personal loans is non-performing. Three point four million people are in a government programme for debts they cannot pay. And the countryside is full of houses with no one in them, listed on bank websites at prices that look like bargains until you understand what happened to the people who built them.

What Thailand Does Not Want You To See

The next time someone tells you property in Thailand is cheap, ask them why. Ask them where the family went. Ask them what happened to the farmer who built that house with money he borrowed at 20 percent a month because no bank would lend to him. Ask them why a country with one of the highest household debt ratios on earth has so many empty houses.

They will not have an answer. Because the answer is the thing Thailand does not want you to see. Not the properties. The properties are right there on the bank’s website. What Thailand does not want you to see is who lost them. And why. And what the system did to make sure it happened.

Frequently Asked Questions

Are foreclosed properties in Thailand actually cheap?

Not in the way most foreign buyers think. The headline prices on bank foreclosure websites are typically 30 to 50 percent above what the property would sell for in a free market. The banks deliberately maintain inflated valuations to avoid booking losses on their balance sheets. Of the eleven foreclosed properties I documented two and a half years ago on Kasikorn Bank’s website, seven are still listed today at essentially the same prices. The reason they have not sold is that the price is not where the market wants it to be. The reason the bank will not lower it is that doing so would trigger mark-downs across every other property on the bank’s books.

What is Thailand’s real household debt ratio?

The official figure is 87 percent of GDP, already one of the highest in the world at seventh globally. The real figure, when informal loans (loan shark debt, pico finance, neighbour-to-neighbour borrowing) are included, is 104 percent of GDP, according to a Chulalongkorn University study commissioned by the Joint Standing Committee for Commerce, Industry and Banking. Forty percent of Thai households carry informal debt. The average informal debt per household is nearly 100,000 baht.

What interest rates do Thai loan sharks charge?

Up to 240 percent per year in rural Thailand. Some charge 20 percent per month. These rates would be criminal in any developed country. They are the rates Thai families turn to when commercial banks tighten lending and refuse to serve the informal sector. Nearly half of all informal borrowing, 47.5 percent, is for daily consumption rather than investment or business, meaning Thai families are borrowing at 240 percent annual interest just to eat.

How many Thai families have non-performing loans?

More than 1.2 trillion baht in loans are currently classified as non-performing in the Thai credit bureau system. The government launched a debt-relief programme targeting 3.4 million people with small NPLs under 100,000 baht. The flagship debt clinic, Sukhumvit Asset Management (SAM), has managed to restructure between 55,000 and 60,000 cases out of millions. The programme barely scratches the surface. Personal loans across the system have a non-performing rate of 10.77 percent.

Why are so many Thai houses sitting empty?

Because the banks refuse to lower the prices to where buyers exist. When a Thai bank repossesses a property, it goes on the balance sheet as a Non-Performing Asset at near the original loan value, not the real market value. Selling at the real market price would trigger mark-downs across the bank’s entire residential portfolio, which would cascade through every other bank’s portfolio, which would expose the fact that the country’s residential property valuations are a shared fiction. So nothing sells. The houses sit. The bank pretends the asset is worth what the website says. The rural Thai family who lost the home is long gone.

Why is rural Thailand worst hit by the debt crisis?

Because rural Thailand runs on informal employment. More than half of all Thai workers are not formally employed. No contract, no social security, no unemployment insurance, no sick pay. When the harvest fails, when drought hits, when illness strikes, there is no safety net, only debt, and the debt almost never goes through a bank. It goes through a loan shark charging 20 percent a month. Government debt-relief measures focus on formal-sector borrowers, leaving rural informal borrowers entirely outside the assistance system. Real wages for the poorest Thai workers (those earning under 7,800 baht per month) have fallen 18.5 percent since before the pandemic.

What is the real story behind cheap Thai property?

The real story is that someone lost a home. The “amazing deal” on the bank website is a Thai family’s life as they knew it ending. The “special promotional price” is a bank refusing to acknowledge that the house was never worth what the bank lent against it. The “rural bargain” is the wreckage of a debt emergency that has been quietly destroying the Thai countryside for over a decade. Cheap property in Thailand is not cheap because the country is a bargain. It is cheap because Thai people are being financially destroyed. And it is not even cheap enough, because the banks will not let the prices fall to where the market actually clears.

Sources

1. Household debt 16.3 trillion baht, 87% of GDP (official)

https://www.nationthailand.com/business/economy/40050996

2. Including informal loans: 104% of GDP — Chulalongkorn University/JSCCIB

https://www.bangkokpost.com/business/general/2935951/

3. 40% of households have informal debt, average 98,538 baht

https://www.bangkokpost.com/business/general/2935951/

4. Loan shark rates up to 240% annually

https://www.khaosodenglish.com/featured/2024/11/25/thai-household-debt-drops-below-90/

5. Shark loans totalled 67 billion baht, 47.5% for daily consumption

https://www.khaosodenglish.com/featured/2024/11/25/thai-household-debt-drops-below-90/

6. NPLs exceed 1.2 trillion baht in credit bureau system

https://gam-legalalliance.com/insights/thailands-household-debt-crisis/

7. Personal loan NPL ratio 10.77%

https://www.nationthailand.com/business/economy/40050996

8. 3.4 million people targeted by debt-relief programme

https://www.oecd.org/en/publications/oecd-economic-surveys-thailand-2025_426b9bc0-en/

9. SAM Debt Clinic: 55,000-60,000 restructured cases

https://gam-legalalliance.com/insights/thailands-household-debt-crisis/

10. Workers under 7,800 baht/month: real income fell 18.5%

https://www.krungsri.com/en/research/research-intelligence/household-wealth-2025

11. Average worker real income growth 0.8% per year since pre-COVID

https://www.krungsri.com/en/research/research-intelligence/household-wealth-2025

12. 40-50% of income spent on debt interest

https://gam-legalalliance.com/insights/thailands-household-debt-crisis/

13. Commercial bank lending contracted 1.2%

https://www.khaosodenglish.com/featured/2024/11/25/thai-household-debt-drops-below-90/

14. Over 50% of workers not formally employed

https://www.imf.org/en/news/articles/2025/04/09/cf-thailand-can-ease-household-debt-burden

15. IMF projects 2% growth 2025, 1.6% 2026

https://www.fastbull.com/news-detail/thailands-household-debt-crisis-a-looming-drag-on-4353572_0

16. Property market coldest period in two decades

https://www.fastbull.com/news-detail/thailands-household-debt-crisis-a-looming-drag-on-4353572_0

17. Car sales dropped 26% in 2024

https://www.fastbull.com/news-detail/thailands-household-debt-crisis-a-looming-drag-on-4353572_0

18. Tourism declined 7.5% YoY first 9 months 2025

https://www.fastbull.com/news-detail/thailands-household-debt-crisis-a-looming-drag-on-4353572_0

19. Debt described as “cancer” not “bomb” by economists

https://gam-legalalliance.com/insights/thailands-household-debt-crisis/

20. 7th highest household debt-to-GDP ratio globally

https://www.fastbull.com/news-detail/thailands-household-debt-crisis-a-looming-drag-on-4353572_0

21. Informal debt: 100,000-200,000 baht per household, 20%+ per month

https://gam-legalalliance.com/insights/thailands-household-debt-crisis/

22. Debt driven by necessity not investment — Bangkok Bank

https://www.fastbull.com/news-detail/thailands-household-debt-crisis-a-looming-drag-on-4353572_0

23. Bank foreclosure listings — Kasikorn, Krungsri, others

https://propertysights.com/articles/buy-bank-foreclosed-assets/

24. Household debt peaked 95.5% GDP March 2021, now ~86-88%

https://www.ceicdata.com/en/indicator/thailand/household-debt–of-nominal-gdp